Published on the 18th January 2024

Does Home Insurance Cover My Personal Belongings?

Reading Time: 5 min read

Knowing if your home insurance policy covers your personal belongings is essential. Many home insurance policies exist, and different providers often cater to different needs. Whether you’re a homeowner or just renting a property, let’s look at personal possessions cover and the considerations needed before agreeing on a premium.

Contents

● Personal Belongings and Contents Insurance

● What Does Contents Insurance NOT Cover?

● Calculating the Cost of Personal Belongings

● What if You’re Away from Your Property?

● Conclusion

Personal Belongings and Contents Insurance

‘Personal belongings’ may be alternatively named ‘possessions’, or ‘personal property’. As the name suggests, these are items that you can insure in addition to taking out building insurance.

Personal belongings may include the likes of a book or vinyl collection, electronic/entertainment equipment, sports equipment, and musical instruments. It also includes any removable items from your home, such as carpets, curtains, air-conditioning and energy-saving equipment, furniture, and fittings for the likes of kitchens and bathrooms. The average home has contents worth in excess of £35,000, so your personal possessions may come to more than you think!

Such items can be insured under the umbrella title of contents insurance. Most of those taking out a house insurance policy will take out both a buildings and contents plan.

For a wider view, read our article on What are the Different Types of Home Insurance?

What Does Contents Insurance NOT Cover?

Personal belongings insurance is not quite as straightforward as it may appear. Firstly, you must inventory your personal possessions and create a fair and accurate total cost. Secondly, if you happen to own any high-value items – such as jewellery, artwork, or designer clothes – you may need to pay an additional premium on top of a contents insurance figure.

If you don’t declare valuable items, your coverage may not include them in case of accidental damage or loss. You may ask, does homeowners insurance cover wear and tear to items, it is usually deemed to be the responsibility of their owner.

Finally, not everything that may be classed as a ‘personal belonging’ will be covered by contents insurance. If you own any motor vehicles, they won’t fall under a house insurance policy, even if it’s kept in a secure garage on the property. Any animals you legally own as pets will also not fall under the ‘personal belongings’ category.

Even though insurance policies can be highly comprehensive, they won’t cover you for all eventualities. Double-check your contents policy details to find out what coverage you have. Our own premiums will guard against the likes of fire, flooding, and theft. However, it’s unlikely that you’ll be able to find coverage against, no matter where you live in the world.

Calculating the Cost of Personal Belongings

It’s really worth taking your time when it comes to calculating the cost of personal items. Put aside a few hours and take a tour around your property, writing down all of the items that have any value. Be sure to include furniture and fittings, and if possible, keep a record of any purchase receipts.

It’s handy to note the year you bought any items and any serial numbers for electronic equipment.

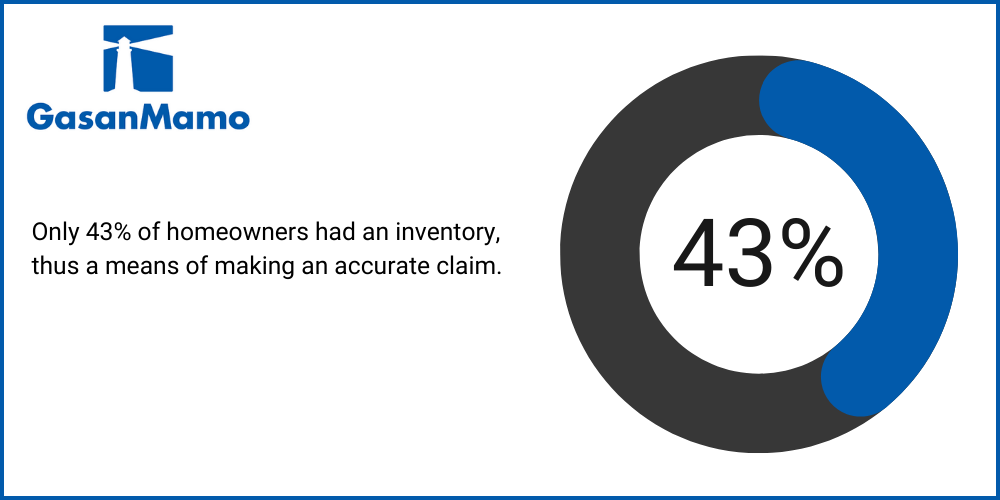

A 2020 consumer poll showed that just 43% of homeowners had an inventory, thus a means of making an accurate claim. Doing this may seem time-consuming, but it will save you time when making a claim at a later date. Having this information will also ensure that you’re paying an accurate premium for your contents insurance.

What if You’re Away from Your Property?

Should a fire or theft occur in your home when you’re at work or on holiday, your contents insurance will still cover the cost of your lost items.

However, if there are items that you’ll regularly be taking outside of your home – such as jewellery, clothes, or musical instruments – notify your insurer in advance.

Regarding a long-term absence from your home, the policies of different providers can differ wildly. Our own insurance will cover you for a generous 90 consecutive days. Once that period has expired, insurance coverage is excluded for oil leaks from fixed heating installations, belongings against loss or damage to valuables and money, and any liability resulting from fraudulent use of credit or debit cards. You should always check your insurance entitlement if you go away for a lengthy period.

Conclusion

When it comes to securing personal belongings insurance via a home insurance policy, contents insurance will cover most of your needs. However, a cautious understanding of any limitations will ensure you pay the right premium amount. You should take the time to inventory your possessions’ costs accurately. You should also ensure that you highlight any expensive items in case an additional payment is required.

Begin your own search for the right plan by looking through our clear and transparent benefits on our home insurance page.

GasanMamo Insurance is authorised under the Insurance Business Act and regulated by the MFSA.